Fundamentals

ETF instead of Futures Contracts

December/20/2009 10:55

Several people have emailed me regarding alternatives to future contracts. The issue is that some people do not feel comfortable with the high-leverage, rolling over futures contracts, etc. Please note that all these techniques (i.e. COT proxy, etc) can be used with ETFs. Below are some important ETFs to know:

- SPY : S&P 500 Index

- DIA : Dow Jones Industrial Average

- QQQQ : NASDAQ Index

- IWM : Russel 2000 Index

- IEV : S&P Europe 350 Index

- EWJ : MSCI Japan Index

- DBA : Agriculture Commodity Index (Corn, Soybeans, Wheat, Sugar)

- US0: Oil

- UGA: Gasoline

- GLD: Gold

- DBB : Aluminum, zinc, copper

- GSC: 24 commodities including energy, agriculture, and precious metals

- UUP : Dollar Bullish

- UDN : Dollar Bearish

- SPY : S&P 500 Index

- DIA : Dow Jones Industrial Average

- QQQQ : NASDAQ Index

- IWM : Russel 2000 Index

- IEV : S&P Europe 350 Index

- EWJ : MSCI Japan Index

- DBA : Agriculture Commodity Index (Corn, Soybeans, Wheat, Sugar)

- US0: Oil

- UGA: Gasoline

- GLD: Gold

- DBB : Aluminum, zinc, copper

- GSC: 24 commodities including energy, agriculture, and precious metals

- UUP : Dollar Bullish

- UDN : Dollar Bearish

Economic Purpose of Future Markets and Fundamentals

November/02/2008 22:20

I have been getting some questions regarding the fundamentals of futures markets. First of all, it is important to understand that commodities and futures do not trade in shares like stocks. They trade in contracts. Each futures contract has a standard size that has been set by the futures exchange it trades on. Each commodity or futures contract is different and have contract specifications. For instance, the contract size for gold futures is 100 ounces, which means when you are buying 1 contract of gold, you are really controlling 100 ounces of gold. Consequently, if the price of gold moves $1 higher, that will affect the position by $100 ($1 x 100 ounces). Commodities and Futures markets are characterized by high leverage (i.e. with a small amount of money -the contract- you control a significantly higher amount of the commodity).

Below are some important excepts from the Education Center of the U.S. Commodity Futures Trading Commission regarding future contracts:

Many people think that futures markets are just about speculating or “gambling.” Futures markets can be used for speculating, but they are designed as vehicles for hedging and risk management so that people can avoid “gambling” if that is not their choice. For example, a wheat farmer who plants a crop is, in effect, betting that the price of wheat won’t drop so low that the farmer would have been better off not planting at all. This bet is inherent to the farming business, but the farmer may prefer not to make it. The farmer can hedge this bet by selling a wheat futures contract. Futures markets can be used for both hedging and speculating.

Forward Contracts

Because a forward contract is similar to a futures contract from an economic standpoint, it is helpful to begin by defining a forward contract. A forward contract is an agreement between two parties (say, a wheat farmer and a breakfast cereal manufacturer) in which the seller (the farmer) agrees to deliver to the buyer (the cereal manufacturer) a specified quantity and quality of an asset or commodity (the wheat) at a specified future date at an agreed upon price. A forward contract can be distinguished from a spot contract, that is, a contract for immediate delivery of the commodity.

A forward contract is typically a privately negotiated bilateral contract that is not conducted on an organized marketplace or exchange. The contract terms are not standardized but are determined by what the parties agree on. The price generally is determined when the contract is entered into, although there are some forward contracts where the parties may agree to transact at a price to be determined later in a manner that is specified on the day the contract is entered into.

Forward contracts are primarily merchandising vehicles, whereby both parties expect to make or take delivery of the commodity on the agreed upon date. It is difficult to get out of a forward contract unless you can get your counterparty to agree to extinguish the contract. To enter into a forward contract, it is also necessary to find someone who wants to buy exactly what you want to sell when and where you want to sell it. As such, forward contracts are commonly used as merchandising vehicles in a variety of commodity and currency markets; however, forward contracts lack certain features that make futures contracts especially useful for hedging.

Futures Contracts

Futures contracts are very similar to forward contracts, but futures contracts typically have certain features that make them more useful for hedging and less useful for merchandising than forward contracts. These include the ability to extinguish positions through offset, rather than actual delivery of the commodity, and standardization of contract terms.

Futures contracts typically are traded on organized exchanges in a wide variety of physical commodities (including grains, metals, and petroleum products) and financial instruments (such as stocks, bonds, and currencies). Before around 1970, most futures trading was in agricultural commodities, such as corn and wheat. Today, successful futures markets exist in a variety of non-agricultural commodities, including metals such as gold, silver, and copper and fossil fuels such as crude oil and natural gas.

The most widely traded futures contracts are in financial instruments, such as interest rates, foreign currencies, and stock indexes. Single-stock futures, banned in the United States for many years, began trading in November 2002.

Traditionally, futures contracts were traded in an open outcry environment where traders and brokers in brightly colored jackets shout bids and offers in a trading pit or ring. While open outcry is still the primary method of trading agricultural and other physical commodity futures in the U.S., trading in many financial futures has been migrating to electronic trading platforms (where market participants post their bids and offers on a computerized trading system). Almost all futures trading outside the U.S. is conducted on electronic platforms.

Standardized terms. Futures contracts have standardized terms that are determined by the exchange, rather than by market participants. Standardized terms include the amount of the commodity to be delivered (the contract size), delivery months, the last trading day, the delivery location or locations, and acceptable qualities or grades of the commodity.

For example, the Chicago Board of Trade (CBOT) wheat futures contract provides for delivery of 5,000 bushels of any of several varieties of wheat during March, May, July, September, or December in Chicago or any of several other specified delivery locations. The exchange specifies that different varieties and grades can be delivered at various fixed differentials (premiums or discounts) to the contract price.

This standardization enhances liquidity, by making it possible for large numbers of market participants to trade the same instrument. This liquidity makes the contract more useful for hedging, but, on the other hand, the standardization reduces the usefulness of a futures contract as a merchandising vehicle.

A Nebraska farmer who wants to deliver wheat to his or her elevator near Omaha, might find the CBOT wheat futures contract useful for hedging, but would not want to make delivery on the futures contract, since the closest CBOT wheat futures delivery point is in St. Louis. Instead, he or she will buy back or offset the contract before the last trading day and sell the wheat on the spot market locally, as they would have if they had not used the futures market. Most futures contracts (by volume) are liquidated via offset and do not result in delivery. The purpose of the physical delivery provision is to ensure convergence between the futures price and the cash market price.

Clearing. Futures trades that are made on an exchange are cleared through a clearing organization (clearing house), which acts as the buyer to all sellers and the seller to all buyers. When you buy or sell a futures contract, you are technically buying from, or selling to, the clearing organization rather than the party with whom you executed the transaction on the trading floor or through an electronic trading platform. Since you ultimately buy and sell from the same party, if you buy a futures contract and subsequently sell it (probably to a different party than you bought it from but technically back to the clearing house), you have offset your position and the contract is extinguished. Compare this to the forward market: If you buy a forward contract and then sell an identical forward contract to a different person, you now have obligations under two contracts—one long and one short.

Margin. Futures traders are not required to put up the entire value of a contract. Rather, they are required to post a margin that is typically between 2 percent and 10 percent of the total value of the contract. Margins in the futures markets are not down payments like stock margins, but are performance bonds designed to ensure that traders can meet their financial obligations.

When a futures trader enters into a futures position, he or she is required to post initial margin of an amount specified by the exchange or clearing organization. Thereafter, the position is "marked to the market" daily. If the futures position loses value when the market moves against it—if, for example, you are buying and the market goes down—the amount of money in the margin account will decline accordingly. If the amount of money in the margin account falls below the specified maintenance margin (which is set at a level less than or equal to the initial margin), the futures trader will be required to post additional variation margin to bring the account up the initial margin level. On the other hand, if the futures position is profitable, the profits will be added to the margin account. Futures commission merchants (FCMs) often require their customers to maintain funds in their margin accounts that exceed the levels specified by an exchange.

The Role of the Speculator

A speculator is one who does not produce or use a commodity, but risks his or her own capital trading futures in that commodity in hopes of making a profit on price changes. While speculation is not considered one of the economic purposes of futures markets, speculators do help make futures markets function better by providing liquidity, or the ability to buy and sell futures contracts quickly without materially affecting the price. Long and short hedgers may not be sufficient to create a liquid futures market by themselves. The participation of speculators willing to take the other side of hedgers' trades adds liquidity and makes it easier for hedgers to hedge.

Types of speculators include:

• Position traders have an opinion about general price trends and will hold a position for several days or weeks.

• Day traders will close out positions by the end of the trading day (and avoid overnight margin calls).

• Scalpers are exchange members who only hold positions for a few minutes or even seconds. These members “make markets,” that is, they post or shout bids and offers for the contract. The bid (the price at which a market maker is willing to buy the contract) is a little bit lower than the offer (the price at which the market maker is willing to sell the contract). For example, the bid for CBOT December wheat might be $3.50 and the offer might be $3.50½. Scalpers endeavor to profit from the difference between the bid and the offer, generally referred to as the bid-ask spread.

Below are some important excepts from the Education Center of the U.S. Commodity Futures Trading Commission regarding future contracts:

Many people think that futures markets are just about speculating or “gambling.” Futures markets can be used for speculating, but they are designed as vehicles for hedging and risk management so that people can avoid “gambling” if that is not their choice. For example, a wheat farmer who plants a crop is, in effect, betting that the price of wheat won’t drop so low that the farmer would have been better off not planting at all. This bet is inherent to the farming business, but the farmer may prefer not to make it. The farmer can hedge this bet by selling a wheat futures contract. Futures markets can be used for both hedging and speculating.

Forward Contracts

Because a forward contract is similar to a futures contract from an economic standpoint, it is helpful to begin by defining a forward contract. A forward contract is an agreement between two parties (say, a wheat farmer and a breakfast cereal manufacturer) in which the seller (the farmer) agrees to deliver to the buyer (the cereal manufacturer) a specified quantity and quality of an asset or commodity (the wheat) at a specified future date at an agreed upon price. A forward contract can be distinguished from a spot contract, that is, a contract for immediate delivery of the commodity.

A forward contract is typically a privately negotiated bilateral contract that is not conducted on an organized marketplace or exchange. The contract terms are not standardized but are determined by what the parties agree on. The price generally is determined when the contract is entered into, although there are some forward contracts where the parties may agree to transact at a price to be determined later in a manner that is specified on the day the contract is entered into.

Forward contracts are primarily merchandising vehicles, whereby both parties expect to make or take delivery of the commodity on the agreed upon date. It is difficult to get out of a forward contract unless you can get your counterparty to agree to extinguish the contract. To enter into a forward contract, it is also necessary to find someone who wants to buy exactly what you want to sell when and where you want to sell it. As such, forward contracts are commonly used as merchandising vehicles in a variety of commodity and currency markets; however, forward contracts lack certain features that make futures contracts especially useful for hedging.

Futures Contracts

Futures contracts are very similar to forward contracts, but futures contracts typically have certain features that make them more useful for hedging and less useful for merchandising than forward contracts. These include the ability to extinguish positions through offset, rather than actual delivery of the commodity, and standardization of contract terms.

Futures contracts typically are traded on organized exchanges in a wide variety of physical commodities (including grains, metals, and petroleum products) and financial instruments (such as stocks, bonds, and currencies). Before around 1970, most futures trading was in agricultural commodities, such as corn and wheat. Today, successful futures markets exist in a variety of non-agricultural commodities, including metals such as gold, silver, and copper and fossil fuels such as crude oil and natural gas.

The most widely traded futures contracts are in financial instruments, such as interest rates, foreign currencies, and stock indexes. Single-stock futures, banned in the United States for many years, began trading in November 2002.

Traditionally, futures contracts were traded in an open outcry environment where traders and brokers in brightly colored jackets shout bids and offers in a trading pit or ring. While open outcry is still the primary method of trading agricultural and other physical commodity futures in the U.S., trading in many financial futures has been migrating to electronic trading platforms (where market participants post their bids and offers on a computerized trading system). Almost all futures trading outside the U.S. is conducted on electronic platforms.

Standardized terms. Futures contracts have standardized terms that are determined by the exchange, rather than by market participants. Standardized terms include the amount of the commodity to be delivered (the contract size), delivery months, the last trading day, the delivery location or locations, and acceptable qualities or grades of the commodity.

For example, the Chicago Board of Trade (CBOT) wheat futures contract provides for delivery of 5,000 bushels of any of several varieties of wheat during March, May, July, September, or December in Chicago or any of several other specified delivery locations. The exchange specifies that different varieties and grades can be delivered at various fixed differentials (premiums or discounts) to the contract price.

This standardization enhances liquidity, by making it possible for large numbers of market participants to trade the same instrument. This liquidity makes the contract more useful for hedging, but, on the other hand, the standardization reduces the usefulness of a futures contract as a merchandising vehicle.

A Nebraska farmer who wants to deliver wheat to his or her elevator near Omaha, might find the CBOT wheat futures contract useful for hedging, but would not want to make delivery on the futures contract, since the closest CBOT wheat futures delivery point is in St. Louis. Instead, he or she will buy back or offset the contract before the last trading day and sell the wheat on the spot market locally, as they would have if they had not used the futures market. Most futures contracts (by volume) are liquidated via offset and do not result in delivery. The purpose of the physical delivery provision is to ensure convergence between the futures price and the cash market price.

Clearing. Futures trades that are made on an exchange are cleared through a clearing organization (clearing house), which acts as the buyer to all sellers and the seller to all buyers. When you buy or sell a futures contract, you are technically buying from, or selling to, the clearing organization rather than the party with whom you executed the transaction on the trading floor or through an electronic trading platform. Since you ultimately buy and sell from the same party, if you buy a futures contract and subsequently sell it (probably to a different party than you bought it from but technically back to the clearing house), you have offset your position and the contract is extinguished. Compare this to the forward market: If you buy a forward contract and then sell an identical forward contract to a different person, you now have obligations under two contracts—one long and one short.

Margin. Futures traders are not required to put up the entire value of a contract. Rather, they are required to post a margin that is typically between 2 percent and 10 percent of the total value of the contract. Margins in the futures markets are not down payments like stock margins, but are performance bonds designed to ensure that traders can meet their financial obligations.

When a futures trader enters into a futures position, he or she is required to post initial margin of an amount specified by the exchange or clearing organization. Thereafter, the position is "marked to the market" daily. If the futures position loses value when the market moves against it—if, for example, you are buying and the market goes down—the amount of money in the margin account will decline accordingly. If the amount of money in the margin account falls below the specified maintenance margin (which is set at a level less than or equal to the initial margin), the futures trader will be required to post additional variation margin to bring the account up the initial margin level. On the other hand, if the futures position is profitable, the profits will be added to the margin account. Futures commission merchants (FCMs) often require their customers to maintain funds in their margin accounts that exceed the levels specified by an exchange.

The Role of the Speculator

A speculator is one who does not produce or use a commodity, but risks his or her own capital trading futures in that commodity in hopes of making a profit on price changes. While speculation is not considered one of the economic purposes of futures markets, speculators do help make futures markets function better by providing liquidity, or the ability to buy and sell futures contracts quickly without materially affecting the price. Long and short hedgers may not be sufficient to create a liquid futures market by themselves. The participation of speculators willing to take the other side of hedgers' trades adds liquidity and makes it easier for hedgers to hedge.

Types of speculators include:

• Position traders have an opinion about general price trends and will hold a position for several days or weeks.

• Day traders will close out positions by the end of the trading day (and avoid overnight margin calls).

• Scalpers are exchange members who only hold positions for a few minutes or even seconds. These members “make markets,” that is, they post or shout bids and offers for the contract. The bid (the price at which a market maker is willing to buy the contract) is a little bit lower than the offer (the price at which the market maker is willing to sell the contract). For example, the bid for CBOT December wheat might be $3.50 and the offer might be $3.50½. Scalpers endeavor to profit from the difference between the bid and the offer, generally referred to as the bid-ask spread.

Using market sentiment to guide trading

October/12/2008 22:48

I will try to answer selected email questions sent by readers of this blog directly on the blog. Due to time constrains I will try to answer between one and three questions per week. A reader of the blog sent me the following question based on the blog entry “Are the brokers, newsletters, and sentiment always wrong?” written on October 10, 2008:

>> “So if I just do the opposite of market sentiment, I'll make lots of $?! That's a nice simple algorithm.”

For those of you with mathematical background I will say that sentiment is typically a necessary condition to excellent buy or sell opportunities but it is not sufficient one. We need other setup techniques to confirm the setup, an entry technique, and an exit technique before we can say we have a trading strategy.

However, the short answer is that even with sentiment alone you are likely to do significantly better than the general public trying to time the market (most people trying to time the market based on news do very poorly and loose money). We use sentiment as one of our six indicators to analyze setup conditions on specific markets. Once we identify that the market is setup (using commercials, large traders, small traders, valuation, seasonality, sentiment, etc), then we still need to go to the daily charts and use a proper entry technique to enter the market and an exit technique to take out the profits.

The chart below shows how we would have done trading the S&P 500 if we had enter the market every time market sentiment went from having been very low to just crossing above the 20% line (i.e. 80% of the brokers, newsletters, etc are recommending “sell, sell, sell”) and exit once sentiment crossed below the 80% line (i.e. 80% of the brokers, newsletters, etc are recommending “buy, buy, buy”). The condition was programmed and the markers appear automatically on the chart as blue up arrows (buy signal) and red down arrows (sell signal). I also show a sample of the profits we would have made if we were trading one contract of the S&P500 future ($17,318.00). Note that we had many trades since 2001 that made 100% profit (i.e. a return of $17,328.00 on an $17,328.00). The reality, however, is that the trading account would need to be larger than $17,328.00 -otherwise we would be risking 100% of it in every trade. We will discuss the concept of “risk-of-ruin” in future entries and on the members area since its is a very important concept for sound money management.

>> “So if I just do the opposite of market sentiment, I'll make lots of $?! That's a nice simple algorithm.”

For those of you with mathematical background I will say that sentiment is typically a necessary condition to excellent buy or sell opportunities but it is not sufficient one. We need other setup techniques to confirm the setup, an entry technique, and an exit technique before we can say we have a trading strategy.

However, the short answer is that even with sentiment alone you are likely to do significantly better than the general public trying to time the market (most people trying to time the market based on news do very poorly and loose money). We use sentiment as one of our six indicators to analyze setup conditions on specific markets. Once we identify that the market is setup (using commercials, large traders, small traders, valuation, seasonality, sentiment, etc), then we still need to go to the daily charts and use a proper entry technique to enter the market and an exit technique to take out the profits.

The chart below shows how we would have done trading the S&P 500 if we had enter the market every time market sentiment went from having been very low to just crossing above the 20% line (i.e. 80% of the brokers, newsletters, etc are recommending “sell, sell, sell”) and exit once sentiment crossed below the 80% line (i.e. 80% of the brokers, newsletters, etc are recommending “buy, buy, buy”). The condition was programmed and the markers appear automatically on the chart as blue up arrows (buy signal) and red down arrows (sell signal). I also show a sample of the profits we would have made if we were trading one contract of the S&P500 future ($17,318.00). Note that we had many trades since 2001 that made 100% profit (i.e. a return of $17,328.00 on an $17,328.00). The reality, however, is that the trading account would need to be larger than $17,328.00 -otherwise we would be risking 100% of it in every trade. We will discuss the concept of “risk-of-ruin” in future entries and on the members area since its is a very important concept for sound money management.

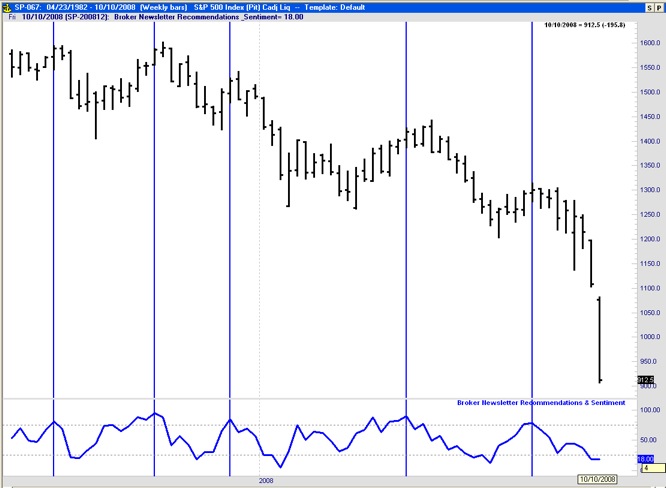

Are the brokers, newsletters, and sentiment always wrong?

October/10/2008 15:19

The chart below shows over a year of the S&P 500 on weekly bars on top (black) and an indicator that measures market sentiment directly from newsletters and broker recommendations at the bottom (blue). You can observe that this guys are consistently wrong. They are very bullish (as shown by indicator values above 80) after significant uptrends and this typically coincides with the end of the trend. Note how in the chart below every time the sentiment indicator went over 80% the market was at a top or very near a top proceeding a significant downtrend. They are consistently very bullish at market highs and very bearish at market lows. Note how once they get very bearish the market is typically close to a bottom also. It is important to emphasize that this behavior is not specific to the S&P500 or this year. I have studied hundreds of out of sample charts and this finding holds true. In the members area I elaborate a little bit more on why this crowd is so wrong and how we can use this information to our advantage.

Methods and Techniques

July/05/2008 23:52

The methods we will use in our evidence-based analysis include:

1) Statistics

2) Classical Time-Series Analysis

3) Complexity Theory

4) Risk-Management

5) Technical Analysis

6) Fundamental Analysis and Valuation

7) Modern Portfolio Theory

8) COT Data

Background of the fundamentals will be provided on the Fundamentals category.

These are the methods we will used primarily when we evaluate trading systems and strategies. We will also use other fundamental techniques to discuss weekly setup conditions for commodity markets.

1) Statistics

2) Classical Time-Series Analysis

3) Complexity Theory

4) Risk-Management

5) Technical Analysis

6) Fundamental Analysis and Valuation

7) Modern Portfolio Theory

8) COT Data

Background of the fundamentals will be provided on the Fundamentals category.

These are the methods we will used primarily when we evaluate trading systems and strategies. We will also use other fundamental techniques to discuss weekly setup conditions for commodity markets.